16 / 160

16 / 160

March

2017

HYDROCARBON

ENGINEERING

14

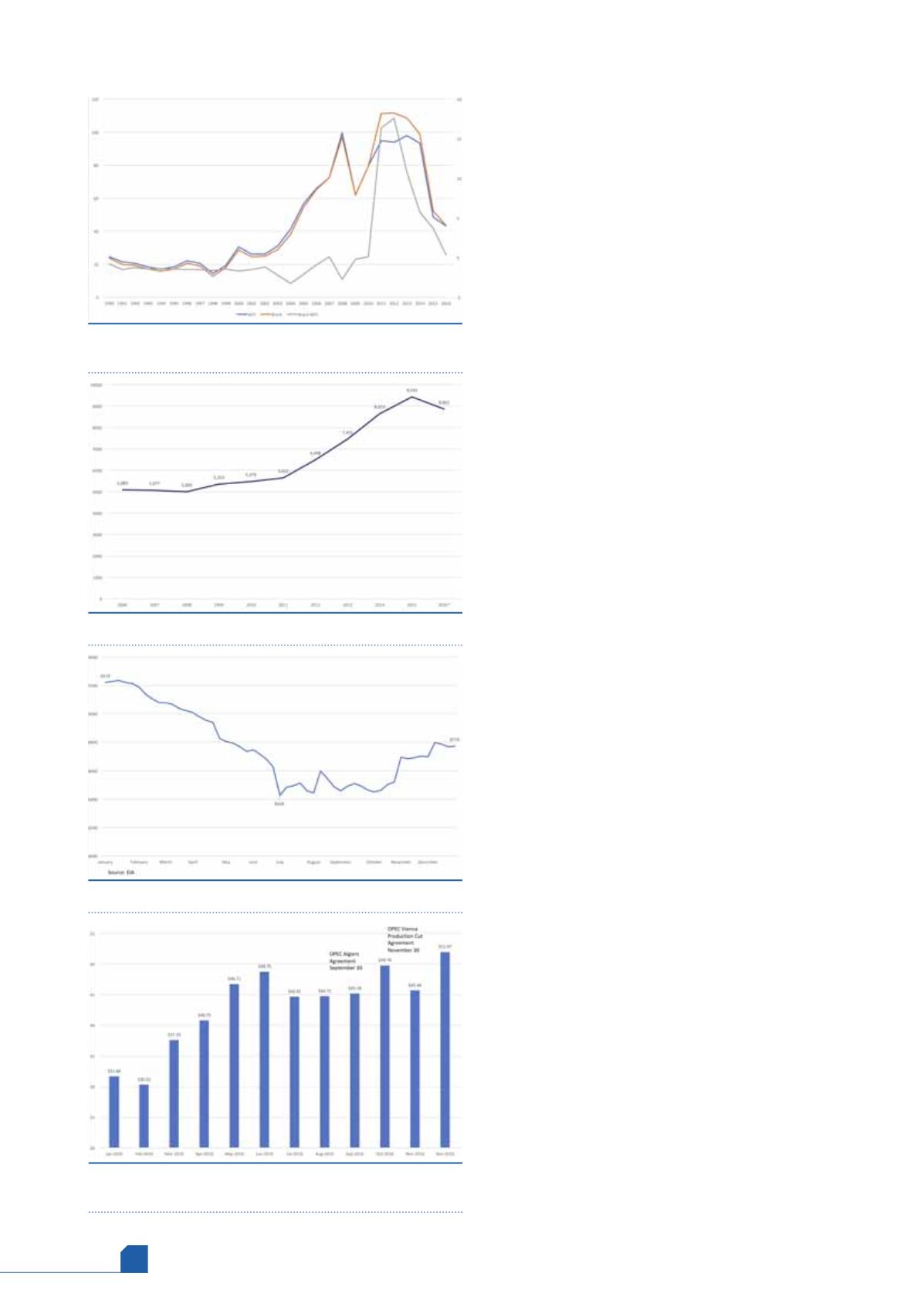

US output of 4.341 million bpd is greater than the total

crude output of any OPEC country other than Saudi Arabia.

Crude prices collapsed in 2009 because of the

recession, but they rose again and hit new highs in

2011 – 2013. At this point, there was an extremely large

price differential between Brent crude and WTI crude. WTI

crude on the spot market was routinely US$15 – 20/bbl

cheaper than Brent crude, though in the past the two

crudes tracked one another closely. This was also related to

the shale boom, since a great deal of new crude was being

produced in landlocked areas, without access to a larger

customer base. Moreover, exports of domestic crude were,

until the end of 2015, restricted (not banned) by federal law.

The easing of restrictions and the logistics of getting crude

to refineries are discussed below.

By late 2014, Saudi Arabia began to raise its output. The

Saudi-led oil price war caused prices to collapse in 2015

and 2016. It was intended to be a war of attrition, where

the higher cost producers would eventually be forced to

exit the market. US shale producers were among the key

targets, since many had relatively high costs of production.

The impact was slow in coming, however, since many US

wells were already drilled and in operation. Over the

course of the oil price war, many US wells closed, and many

companies went out of business. The US producers

remaining worked to increase their drilling efficiency and

cut costs. Still, in 2016, the low prices caught up, and US

production fell to approximately 8.862 million bpd.

The market changed again in late 2016, when 11 OPEC

countries and 11 select non-OPEC countries agreed to

reduce crude production to whittle down global stockpiles

and put crude prices on an upward track. It appeared also

that global demand would finally begin to catch up with

supply in 2017. Already, US producers appear to be

benefitting from the new price cycle. Figure 3 sheds more

light on this by presenting the trend in US crude

production, according to weekly supply data during the full

course of 2016. At the start of 2016, US crude production

was 9.219 million bpd. It fell to a low of 8.428 million bpd in

July. But anticipation of a better supply-demand balance,

combined with the survival of the most efficient US

producers, brought an unexpected end to the downturn in

production. Production was flat-ish for the next few

months until autumn.

OPEC surprised market watchers when it made its

production cut pact in Algiers in late September. The OPEC

regular meeting was held in Vienna, Austria, on

30 November, and the group surprised the market once

again by cementing the production cut agreement.

Additional support was gained in December when

11 non-OPEC countries, including Russia, joined the effort

by pledging to reduce output and/or allow natural declines

in production to continue. The impact on the market has

been dramatic.

Figure 4 shows the monthly average spot price for WTI

crude. In September, the spot price averaged US$45.18/bbl.

It jumped to US$49.78/bbl in October, after the Algiers

Agreement was made. The price then dropped to an

average of US$45.66 in November, when it seemed

impossible that OPEC would manage to get an agreement

Figure 1.

Annual average WTI and Brent spot prices, and

the Brent-WTI differential (US$/bbl).

Figure 2.

US crude production ('000 bpd).

Figure 3.

US crude production, weekly ('000 bpd).

Figure 4.

WTI monthly average spot price, Cushing

(US$/bbl).